Your local bank manager likely sees a vintage chassis and thinks “depreciating asset,” yet the 2026 market values high-end restomods as tangible, appreciating investments. Vintage aesthetics. Modern power. It’s a duality that most traditional lenders simply cannot compute. You understand that a vehicle featuring an LS3 crate engine and a hand-stitched interior is a masterpiece of modern engineering, not a weekend project. Securing classic car financing shouldn’t feel like a battle against a bureaucracy that doesn’t know a dual-exhaust roar from a vacuum leak.

We agree that your capital should work as hard as your Coyote-powered beast. This guide empowers you to master collector car loans, ensuring you obtain low-interest, long-term funding that respects the unrivaled craftsmanship of an Elite Certified build. We will explore how to identify specialized lenders who recognize bespoke value, leverage the investment-grade nature of your vehicle, and create a seamless path from the initial design phase to the first turn of the key.

Key Takeaways

- Understand why standard depreciation-based loans fail and how specialized lenders view your high-value restomod as an appreciating asset.

- Learn to bridge the valuation gap by leveraging modern performance components like LS3 and Coyote engines to secure higher loan amounts.

- Navigate the 2026 lending landscape to identify the best classic car financing options, balancing funding speed with specialized collector-car expertise.

- Identify the specific credit scores and financial markers needed to unlock elite interest rates for your next investment-grade build.

- Discover how “Elite Certified” standards provide a streamlined path to capital by aligning your project with lenders who understand bespoke craftsmanship.

Understanding Classic Car Financing vs. Standard Auto Loans

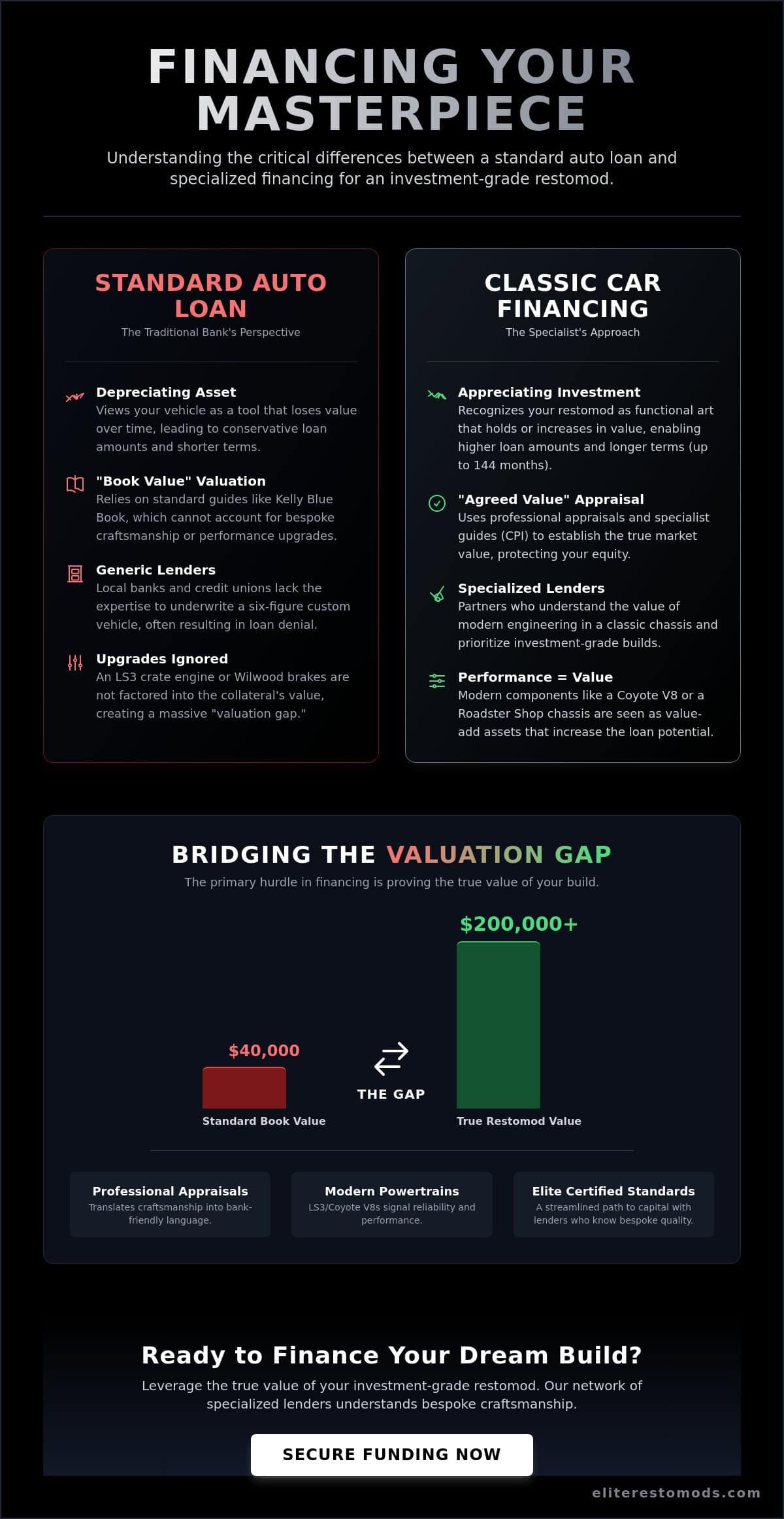

Buying a high-performance restomod isn’t like picking up a commuter car from a local lot. It’s an investment in a bespoke piece of functional art. While a standard auto loan assumes your vehicle is a depreciating tool, classic car financing operates on the premise that your asset will appreciate. These specialized loans treat a 1970 Chevelle with a modern LS3 crate engine as a collateralized investment rather than a liability. Classic style. Modern power. This duality requires a lender who understands that the value of the build often exceeds the original MSRP by six figures.

By 2026, the lending market has undergone a significant transformation. Financial institutions now prioritize performance-ready restomods over static museum pieces. They recognize that a vehicle with modern fuel injection, updated suspension, and reliable cooling systems is a safer bet for a 144 month term. Before diving into the specifics of a loan, it’s helpful to understand the foundational definition of what is a classic car to see how lenders categorize these high-value assets.

To better understand the nuances of these financial products, watch this helpful video:

The Mechanics of Collector Car Equity

Standard loans use “Actual Cash Value,” which is a race to the bottom. Specialized lenders use “Agreed Value.” This ensures that if a total loss occurs, you receive the full amount documented in your appraisal. It’s a synergy between financing and insurance that protects your equity. Many high-net-worth buyers choose to finance even when they have the cash. It’s about liquidity preservation. Why tie up $250,000 in a build when you can secure a 12 year term with low monthly payments and keep your capital in higher-yield investments?

Standard Banks vs. Specialized Lenders

Don’t expect a local credit union to understand the premium on a “fully sorted” 1967 Mustang. They rely on Kelly Blue Book, which has no category for a pro-touring masterpiece. Specialized lenders utilize the CPI (Cars of Particular Interest) guide and custom appraisals to provide classic car financing that reflects true market value. They understand the value of a Coyote engine swap or a hand-stitched interior. When you’re ready to browse current inventory, you’ll see why a generic bank’s valuation falls short. These lenders see the soul of the machine and the meticulous engineering behind it.

Financing the Restomod: Bridging the Valuation Gap

The primary hurdle in classic car financing isn’t your credit score; it’s the “valuation gap.” A standard 1967 Mustang might carry a book value of $40,000 in a traditional appraisal guide. However, a world-class restomod often represents an investment exceeding $200,000. Lenders who rely on legacy depreciation tables see a massive risk where we see a bespoke asset. To bridge this gap, you must move beyond “book value” and into the realm of replacement cost and documented performance. Professional appraisals act as the essential bridge, translating the raw power and meticulous craftsmanship of a build into a language underwriters can trust.

Modern components are the secret weapon in justifying higher loan amounts. When a vehicle features an LS3 crate engine or a 5.0L Coyote V8, it’s no longer just a vintage car. It’s a high-performance machine with measurable reliability. Lenders in 2026 are increasingly recognizing these components as “value-add” assets. A Wilwood braking system or a bespoke chassis isn’t just an upgrade; it’s a safety and longevity insurance policy that protects the lender’s collateral. This “Investment-Grade” designation signals to the bank that the vehicle is a blue-chip asset capable of holding or increasing its value over time.

Valuing Modern Performance in a Vintage Shell

Quantifying the value of a bespoke chassis goes beyond the price of the steel. A Roadster Shop SPEC chassis transforms the ride quality from a floating antique to a precision instrument. In 2026, underwriters look for “turn-key reliability” as a primary metric for loan approval. They want to know the car will start every time, which significantly reduces the risk of the asset sitting idle and depreciating. By documenting the build story through every stage of the restoration, you provide the forensic evidence needed to prove the vehicle’s true worth. This narrative turns a collection of parts into a cohesive, high-value investment.

The Role of Elite Certification in Financing

Investment-grade vehicles demand a higher standard of proof. This is where rigorous quality assurance processes become vital for securing favorable terms. Understanding the classic car loan requirements is the first step, but Elite Certification provides the final push. It ensures the vehicle is “fully sorted,” meaning every mechanical and aesthetic detail has been vetted for perfection. This level of transparency allows lenders to offer higher loan-to-value (LTV) ratios because the risk of “hidden” issues is virtually eliminated. Elite Certification is a standardized metric for restomod excellence that bridges the gap between a builder’s passion and a banker’s spreadsheet. If you’re ready to see how these standards translate to the road, browse our current inventory of precision-engineered classics.

Comparing Classic Car Loan Options for 2026

Securing a high-performance restomod requires a financial strategy as precise as a fuel-injection map. You aren’t just buying a car; you’re acquiring an investment-grade asset that blends vintage soul with modern muscle. Because these vehicles often exceed standard book values, traditional bank loans rarely suffice. Collectors must evaluate different classic car financing options to find a structure that respects the vehicle’s appraised value rather than its original MSRP.

Hobby-Specific Lenders (Woodside, Grundy, etc.)

Specialized lenders like Woodside Credit or Grundy understand that a 1969 Camaro with a modern LT4 swap is worth significantly more than a stock survivor. These institutions offer terms that traditional banks won’t touch, including extended durations up to 180 months. This reduces monthly out-of-pocket costs, though it requires a disciplined approach to equity. Most hobby-specific classic car financing programs require a down payment between 10% and 20%. They also mandate strict usage tiers, often capping annual mileage at 2,500 to 5,000 miles, and require the vehicle to be stored in a fully enclosed, locked garage. This path is ideal for the long-term collector seeking classic car restomods for sale who prioritizes low monthly payments over total flexibility.

Portfolio and Home Equity Options

High-net-worth individuals often bypass traditional automotive debt entirely by using asset-backed or margin loans. By leveraging a brokerage account, a buyer can access immediate liquidity without triggering a taxable event from selling stocks. These loans offer unrivaled speed, allowing you to strike quickly when a bespoke build hits the market. However, 2026 market conditions make variable rates a calculated risk. While margin loans provide agility, the stability of fixed-rate classic car financing protects against sudden shifts in the prime rate. Some collectors still look toward home equity lines of credit, though the interest is generally only deductible if the funds are used for home improvements. Always consult a tax professional before using real estate or stock equity to fund a six-figure automotive acquisition.

For those who prefer speed without collateral, personal unsecured loans are a viable alternative for buyers with credit scores above 740. These provide total freedom of movement; there are no mileage limits and no requirements for enclosed storage. The tradeoff is a higher interest rate and shorter terms, typically capped at 60 or 72 months. Business owners might also explore lease-to-own programs. These can offer significant tax advantages under Section 179 if the vehicle serves a legitimate promotional or corporate purpose, providing a sophisticated way to transition from a lease into full ownership at the end of the term. To fully understand the mechanics behind each of these structures, a deeper look at how do classic car loans work reveals the specific terms, rates, and lender criteria that separate specialty financing from conventional automotive debt.

Classic Car Loan Requirements: How to Get Approved

Securing classic car financing for a six-figure restomod requires more than just a passion for vintage steel. Lenders in 2026 view these vehicles as high-performance investment assets, not depreciating transport. To qualify for the most competitive rates, a credit score of 700 or higher is the functional baseline. High-tier lenders often look for automotive depth; this means a history of successfully managing similar high-value vehicle loans in the past. If your credit profile is thin, even a high income might not satisfy a specialized underwriter.

Debt-to-income (DTI) ratios play a critical role in the approval process. Most specialized lenders prefer a DTI below 40% when factoring in the new monthly payment. They want to ensure your lifestyle can support the maintenance and storage of a bespoke machine without financial strain. Precision meets passion here. You aren’t just buying a car; you’re acquiring a piece of functional art, and your financial profile must reflect that level of responsibility.

Preparing Your Financial Profile

Gathering your documentation early ensures a seamless experience. You’ll need tax returns from the last two years, recent pay stubs, and a clear breakdown of your liquid assets. Understanding how to meet classic car loan requirements involves proving that your financial foundation is as solid as the chassis of your future car. A 20% down payment serves as the standard industry benchmark for restomods, providing the equity cushion lenders demand for custom builds. This skin in the game reduces the lender’s risk and often unlocks lower interest rates.

The Appraisal and Inspection Phase

The appraisal is where the vintage aesthetics of the past meet the modern valuations of today. Lenders require a third-party valuation from a certified appraiser who understands the nuances of the restomod market. A standard blue-book value won’t suffice. The appraisal must account for the LS3 crate engine, the Wilwood braking system, and the thousands of hours of expert labor involved in the build.

Elite Restomods assists this process by providing a comprehensive Proof of Build package. This documentation includes detailed spec sheets and build photos that verify the vehicle is fully sorted and ready for the open road. Lenders also mandate Agreed Value insurance coverage as a non-negotiable condition. This specific type of policy ensures that if a total loss occurs, you’re covered for the full appraised value, not just a depreciated market average. It’s the only way to protect a high-performance investment effectively. Before committing to a loan, working with a professional classic car sourcing service ensures the vehicle you’re financing has been rigorously vetted for hidden mechanical issues before the appraisal ever begins.

Ready to see the level of craftsmanship that lenders trust? Explore our build process to see how we document every step of your car’s transformation.

The Elite Advantage: Financing Your Dream Build

Securing a six-figure masterpiece requires a financial strategy as precise as the tolerances on our LS3 crate engines. At Elite Restomods, we’ve refined the acquisition process to ensure that classic car financing is a seamless extension of the build itself. We don’t just provide a vehicle; we provide a clear path from the first spark of inspiration to the moment you turn the key. Classic style. Modern power. We handle the friction so you can focus on the drive.

Our team acts as your dedicated advocate, streamlining the transition from sourcing a donor chassis to securing a competitive rate. Because our builds are recognized for their engineering excellence, lenders view an Elite vehicle as a high-value asset rather than a speculative project. This distinction is vital for collectors who want to preserve liquidity while expanding their garage with investment-grade machinery. We treat every transaction with the same perfectionism we apply to our hand-stitched interiors.

Strategic Partnerships with Specialized Lenders

We maintain deep-rooted relationships with the industry’s most aggressive specialized lenders. These institutions understand the nuances of the 2026 market and the specific value of an Elite Certified build. While traditional banks might hesitate at the sight of a 1969 Camaro, our partners see a bespoke vehicle equipped with Wilwood brakes, modern suspension, and turn-key reliability. This understanding allows for 24-hour pre-approval windows and loan structures that reflect the true classic car financing needs of modern collectors. Our reputation for unrivaled craftsmanship gives finance houses the confidence to offer terms that recognize the premium performance of our cars. You can explore our current inventory to see the level of detail that our financial partners are eager to back.

Finalizing Your Acquisition

Once the financing is secured, our concierge team manages the heavy lifting. We coordinate the intricate details of title transfers, state-specific tax requirements, and enclosed white-glove transport. One of the primary benefits of our process is the possibility of turn-key ownership; in many cases, you can finalize the drive home while the trailing paperwork is completed. We ensure your new asset is protected, and we can provide guidance on climate controlled car storage to ensure your investment remains in a flawless, museum-quality state. The goal is a transition that is as smooth as a Coyote-powered sprint. You shouldn’t have to wait months to enjoy the roar of the exhaust. When the time eventually comes to sell, leveraging professional classic car consignment services ensures your investment-grade vehicle reaches a global stage of qualified buyers rather than a digital marketplace of tire-kickers. Start the process by reviewing our available builds and taking the first step toward ownership. Contact our team today to discuss your financing options.

Secure Your Automotive Legacy

Vintage aesthetics. Modern power. Owning a bespoke restomod is more than a purchase; it’s a strategic investment in functional art. Navigating classic car financing in 2026 requires understanding the valuation gap between a standard 1967 Mustang and a performance machine featuring a 460-horsepower Coyote engine. Traditional banks often rely on 20-year-old depreciation models. Our specialized partners recognize the intrinsic value of high-performance upgrades and Elite Certified Quality Assurance. We bridge the gap by curating investment-grade vehicles that meet the rigorous standards of top-tier collector lenders. You’ve spent years dreaming of the roar from a 6.2L LS3 crate engine. Now, with the right financial structure in place, that dream becomes a tangible reality. Our team ensures every meticulous detail, from the hand-stitched leather to the Wilwood braking system, is accounted for in your appraisal. Don’t let outdated lending criteria stall your journey. The marriage of brute force and refined comfort is within your reach.

Explore our inventory and financing options

Your seat in the cockpit is waiting.

Frequently Asked Questions

How do classic car loans differ from standard auto loans?

Classic car loans differ from standard financing by utilizing an “Agreed Value” model rather than “Actual Cash Value.” Standard lenders expect a vehicle to lose 15% of its value annually. In contrast, specialized classic car financing recognizes that a 1969 Camaro with a 650-horsepower LT4 crate engine is a bespoke investment that appreciates. These loans often feature lower interest rates and longer repayment windows to accommodate the high-tier status of these functional art pieces.

Can I finance a restomod with a modern engine swap?

You can absolutely finance a restomod featuring a modern engine swap through specialized collector car lenders. While traditional banks struggle to value a vintage chassis paired with a 2026-spec Coyote V8 or Wilwood braking system, specialty firms prioritize the build quality. They evaluate the professional restoration and performance upgrades as value-adds. This ensures your investment in modern reliability and vintage aesthetics is fully protected under the loan agreement.

What is the typical down payment for a classic car loan?

A typical down payment for a high-performance restomod ranges from 10% to 20% of the purchase price. For an investment-grade vehicle valued at $150,000, expect to provide $15,000 to $30,000 upfront. This equity stake secures your position and often unlocks more favorable interest rates. Lenders require this commitment to ensure the borrower is invested in the long-term preservation of the vehicle’s flawless finish and mechanical integrity.

Are there mileage restrictions on financed classic cars?

Most specialized lenders impose annual mileage limits ranging from 2,500 to 5,000 miles to preserve the vehicle’s investment value. These constraints ensure the car remains a well-maintained collector piece rather than a daily commuter. However, 2026 market trends show an increase in “freedom tier” policies that allow for higher mileage. These flexible options cater to owners who want to hear the roar of their LS3 on more frequent cross-country excursions.

What credit score do I need for classic car financing in 2026?

Lenders generally require a minimum credit score of 700 for classic car financing; however, scores above 740 secure the most competitive 2026 rates. Because these are considered luxury assets rather than essential transportation, underwriters look for a robust credit history. They prioritize borrowers with a proven track record of managing high-limit installment loans. A Tier 1 credit profile reflects the same meticulous attention to detail found in a hand-stitched leather interior.

Can I use a personal loan to buy a classic car?

You can use an unsecured personal loan to purchase a vintage vehicle, but these typically carry interest rates 3% to 5% higher than secured collector car loans. Personal loans don’t require the vehicle as collateral, which simplifies the process but lacks the “Agreed Value” protection. For a bespoke restomod, a dedicated classic car loan is usually superior. It ensures the financing structure matches the true market value of the engineering and craftsmanship.

How long are the terms for a collector car loan?

Loan terms for investment-grade classics frequently extend to 120 or 144 months. These 10 to 12-year durations are significantly longer than the 60-month terms typical of modern daily drivers. This extended timeline keeps monthly payments manageable while you enjoy the unrivaled performance of your build. It treats the car as a long-term asset, allowing the vehicle’s market appreciation to outpace the loan’s principal balance over time.

Does the car need to be appraised before financing is approved?

A professional appraisal is mandatory for nearly all classic car financing agreements to verify the vehicle’s condition and build quality. Lenders require a certified specialist to document the mechanical upgrades, such as a custom chassis or modern fuel injection. This 2026 standard protects both the lender and the buyer. It confirms that the iconic silhouette of the car is backed by the modern engineering and reliability promised in the build story.