Acquiring a high-performance restomod is no longer just an emotional pursuit. It’s a calculated deployment of capital that requires the same precision as the hand-built engine under the hood. Vintage soul. Modern capability. You likely recognize the frustration of presenting a bespoke masterpiece to a traditional lender only to have them ignore the artisanal craftsmanship and modern performance upgrades. Securing financing a six-figure classic car shouldn’t mean settling for an appraisal that misses the mark or interest rates that fail to account for the reliability of modern engineering.

This guide will help you bridge the gap between nostalgia and modern investment strategy. You’ll master the complexities of high-value automotive lending to secure your investment-grade restomod with sophisticated capital strategies that recognize the full market value of elite builds. We’ll explore the shifting 2026 lending environment, covering everything from USPAP-compliant appraisal standards to extended terms that preserve your liquidity. It’s time to ensure your financial structure is as refined as your vehicle’s hand-stitched interior.

Key Takeaways

- Understand why the 2026 market treats elite restomods as recognized asset classes rather than simple hobbyist projects.

- Discover how financing a six-figure classic car serves as a sophisticated hedge against inflation while preserving your liquid capital.

- Identify the specific credit expectations and down payment strategies required to secure favorable terms from specialty lenders.

- Learn to navigate the appraisal hurdle by utilizing certified experts who value modern performance engineering over basic VIN data.

- Explore how a specialized referral network and certified build process can streamline the underwriting journey for bespoke acquisitions.

The Landscape of Financing a Six-Figure Classic Car in 2026

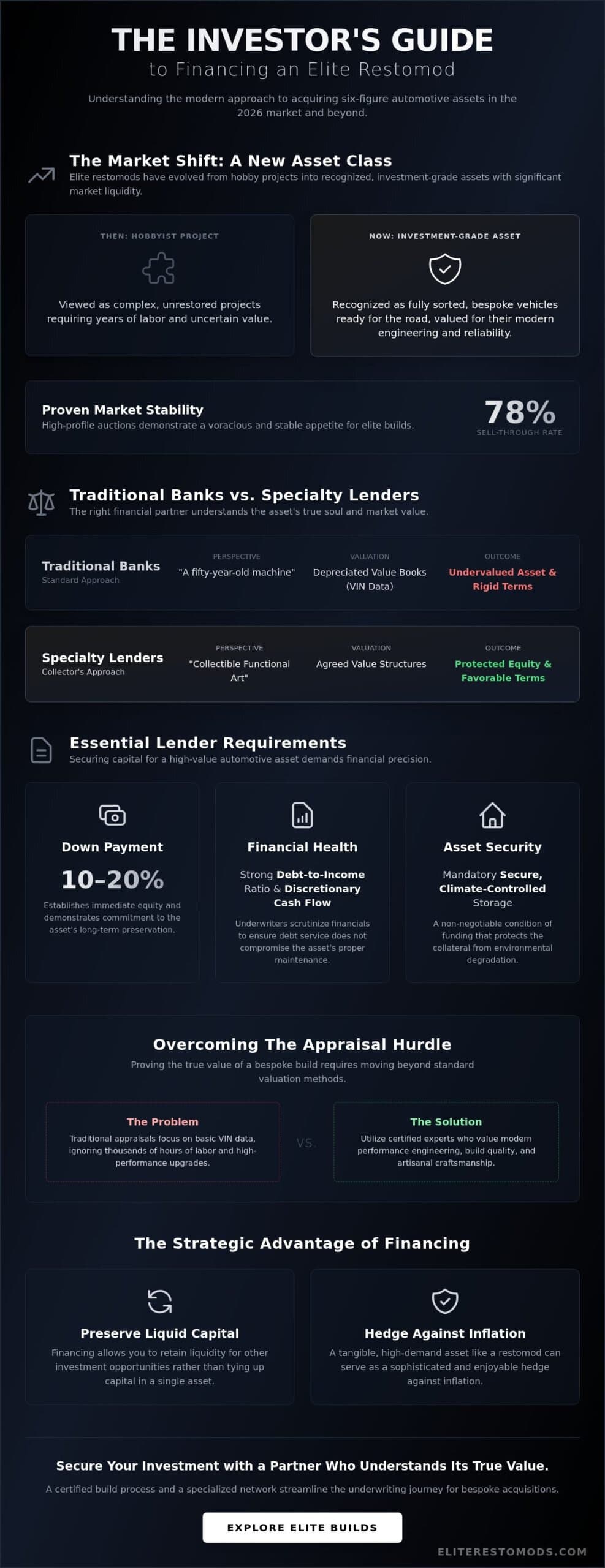

The collector car market has reached a sophisticated tipping point. It’s a space where raw, visceral power meets calculated financial diversification. The six-figure restomod has officially moved past the era of the garage-built hobby project. It’s now a recognized asset class. Investors and enthusiasts alike are pouring capital into vehicles that offer the silhouette of a legend but the heartbeat of a modern supercar. This transition has fundamentally altered how lenders view these machines. They aren’t just old cars anymore. They are bespoke pieces of functional art with significant market liquidity.

Modern collectors prioritize the fusion of heritage aesthetics with contemporary performance engineering. While Wikipedia’s definition of a vintage car typically focuses on chronological age and historical eras, the 2026 market values the developmental narrative of the build. This shift in perception is critical for anyone considering financing a six-figure classic car. Lenders now look for the quality of the components and the reputation of the builder as much as the VIN itself. The six-figure threshold represents the moment where custom engineering meets investment-grade rarity.

To better understand the practical side of this financial journey, watch this helpful video:

The Shift Toward Investment-Grade Restomods

Modern reliability has fundamentally increased the collateral value of classic silhouettes. A fuel-injected Coyote engine or a precision-tuned LS3 provides a level of operational certainty that traditional vintage engines lack. Lenders appreciate this. High-profile auctions in early 2026 showcased a stable 78% sell-through rate, proving that the appetite for elite builds remains voracious. The market now favors vehicles that are fully sorted and ready for the open road. Collectors are moving away from unrestored projects that require years of labor. They want the finished product. They want the immediate experience of the drive.

Traditional Banks vs. Specialty Lenders

Most traditional banks fail to grasp the nuance of a $150,000 vintage Bronco or a bespoke Mustang. They consult depreciated value books and see a fifty-year-old machine. They don’t see the artisanal interior or the high-performance chassis. Specialty lenders are different. They treat these vehicles as collectibles rather than depreciating assets. They utilize agreed value structures that protect your equity from day one. This distinction is vital when financing a six-figure classic car. While a standard credit union might offer rigid terms, specialty partners understand the soul of the asset. You can explore our current inventory to see the level of craftsmanship that these specialized financial products are designed to support.

Essential Lender Requirements for High-Value Automotive Loans

Securing capital for a mechanical masterpiece requires more than just a passion for the open road. It demands financial precision. When financing a six-figure classic car, lenders move beyond standard risk models to evaluate the borrower as a curator of high-value assets. Most specialty institutions require a down payment ranging from 10% to 20% to establish immediate equity. This initial stake reduces lender exposure and demonstrates your commitment to the vehicle’s long-term preservation. It’s a fundamental step in aligning your interests with the financial partner backing the acquisition.

The underwriting process for these elite machines is rigorous. Lenders scrutinize debt-to-income ratios with a focus on discretionary cash flow, ensuring the debt service doesn’t compromise the owner’s ability to maintain the asset. Beyond the numbers, the physical security of the vehicle is paramount. Most high-value loan agreements include a mandate for secure, climate-controlled storage. This isn’t just a suggestion. It’s a condition of funding designed to protect the collateral from environmental degradation and market volatility. If you are still in the planning stages, exploring our professional automotive services can help you prepare the necessary infrastructure for a successful approval.

The Importance of a Tier 1 Credit Profile

A pristine credit history is the primary lever for unlocking favorable terms. In the 2026 market, a score of 740 or higher is typically required to access the most competitive capital. For instance, data from March 2026 indicates that borrowers with 750+ scores can secure rates as low as 5.49% for 36-month terms, though 72-month loans often range between 6.99% and 9.49%. Maintaining this Tier 1 status is essential for securing extended terms that can reach up to 180 months, allowing for lower monthly payments while you enjoy the vehicle’s appreciation.

Documentation and Provenance

Traditional banks often struggle to value a bespoke build because they lack a mechanical biography. A fully documented build history is non-negotiable for six-figure approvals. This includes a comprehensive build book featuring professional photography, a detailed list of high-performance components, and receipts from recognized builders. Elite Certified Restomods carry significant weight with underwriters because they represent a known standard of excellence. This level of transparency bridges the gap between a generic VIN and the true market value of the craft.

Storage and Insurance Mandates

Lenders require proof that the asset is protected by agreed value insurance rather than standard actual cash value policies. This ensures that the full investment is covered in the event of a total loss. You can find more detail on these specific lender requirements for classic car financing through industry guides that highlight the necessity of professional appraisals. Utilizing climate-controlled car storage is often the final piece of the puzzle, providing the lender with the confidence that the vehicle’s artisanal interior and mechanical intricacies will remain in showroom condition throughout the life of the loan.

Strategic Leverage: Financing vs. Cash for the Modern Collector

Strategic capital allocation is what separates a casual enthusiast from a world-class curator. While the impulse to pay cash for a high-value asset is understandable, it’s often the least efficient path for a modern collector. Financing a six-figure classic car allows you to maintain liquidity while enjoying a bespoke piece of functional art. It’s about leverage. It’s about preserving your principal for opportunities that offer higher yields than the cost of automotive debt. In an era where market dynamics shift quickly, holding a low-interest loan against an appreciating, high-performance asset acts as a powerful financial hedge. You aren’t just buying a car. You’re managing an investment portfolio.

The psychological benefit of low monthly payments cannot be overlooked. Instead of a massive six-figure capital outlay that disappears from your balance sheet, a structured loan preserves your cash flow. This approach allows you to enjoy the visceral thrill of a 500-horsepower restomod without the “all-in” anxiety of a cash purchase. It’s a sophisticated way to play the long game. You keep your capital working in real estate or equities while the vehicle sits in your garage, potentially appreciating as the market for elite builds remains resilient.

The Opportunity Cost of Liquidity

The math is simple. If your investment portfolio yields 8% to 12% annually, and you can secure a specialty loan at 6.99% to 9.49%, the spread works in your favor. Tying up $150,000 in a single automotive asset creates a significant opportunity cost. By utilizing 180-month terms, you can dramatically reduce the impact on your monthly cash flow. This long-term amortization schedule is a tool used by savvy collectors to acquire investment-grade assets without disrupting their broader financial strategy. Even as the broader market saw a 6% correction in early 2026, high-end, fully sorted builds continue to command premium prices due to their rarity and engineering excellence.

Financing as an Acquisition Tool

Leverage changes your perspective on what is possible. It’s the difference between settling for a $75,000 “driver” and owning a $150,000 Elite Certified masterpiece. Strategic lending allows you to move up into a higher tier of vehicle that a strict cash budget might not allow. This is particularly important when rare inventory hits the market. Having a pre-approval in place means you can act with the speed of a cash buyer but with the strategic advantage of a financed acquisition. You can view our current classic car restomods for sale to see the caliber of inventory that becomes accessible through these sophisticated capital moves. When the right car appears, your financial structure should be as ready as the vehicle itself.

The Appraisal Hurdle: Proving Value in a Bespoke Market

The appraisal is where many high-value acquisitions stall. Standard valuation guides like NADA or KBB are built for stock survivors and mass-market commuters. They are fundamentally irrelevant for the six-figure restomod market. A lender looking at a black-book value for a 1969 Camaro will see a fraction of the build cost. Bridging this gap requires an independent appraisal that focuses on build quality rather than just the VIN. Financing a six-figure classic car becomes a technical argument where hardware justifies the price tag. You aren’t just buying a vintage silhouette. You’re buying a modern supercar in a classic shell.

Modern components carry specific, quantifiable market values that must be accounted for by the lender. A precision-engineered LS3 crate engine or a Roadster Shop chassis represents tens of thousands of dollars in tangible value. When these elements are combined with artisanal craftsmanship, the vehicle moves into a different asset class. Overcoming the “comparable sales” challenge for one-of-one custom builds requires a builder with a track record of high-value sales. This established reputation provides the data points that underwriters need to approve six-figure capital allocations.

Navigating the Valuation Gap

Educating the lender is paramount. You aren’t buying a project car. You’re buying a performance asset. A component-by-component breakdown provides the transparency underwriters crave. By showing the mechanical intricacies, from the Wilwood braking system to the bespoke electrical architecture, you transform a generic loan request into a professional asset acquisition. You can see the level of detail we provide to lenders and appraisers on our build process page. This documentation ensures the lender sees the same value that you do.

The Power of Professional Consignment Data

In a one-of-one market, finding direct “comps” is difficult. This is where professional consignment data becomes a strategic weapon. Utilizing sales figures from elite auctions and private placements helps stabilize the valuation in the eyes of the bank. In early 2026, the global sell-through rate at classic car auctions stabilized at 78%, signaling a healthy demand for top-tier assets even as mid-tier markets cooled. A “fully sorted” certification from a master builder acts as a seal of approval for appraisers. It confirms that the vehicle is ready for the road, not just the showroom. If you are looking to establish a market-ready valuation for your own vehicle, our Consignment Program provides the professional data needed to satisfy the most rigorous lending requirements.

Securing Your Investment with Elite Restomods

The transition from a sophisticated capital strategy to the visceral reality of the open road is where our expertise as curators truly shines. We understand that acquiring an investment-grade icon is a transformative journey. It requires more than just a transaction; it demands a partnership. Our specialized referral network for financing a six-figure classic car connects you with lenders who share our deep appreciation for high-performance engineering. These partners don’t just see a vintage chassis. They see the precision of a modern drivetrain and the artisanal value of a bespoke build. This synergy ensures that your financial structure is as robust as the machine it supports.

We’ve designed our Elite Certified process to remove the friction from the underwriting journey. By providing a transparent, mechanical biography for every vehicle, we give lenders the confidence they need to approve high-value capital allocations. It’s about proving the integrity of the asset. Our builds are recognized for their reliability and craftsmanship, which simplifies the appraisal process and helps you secure the terms you deserve. Every detail is meticulously documented. This ensures your investment is recognized and protected from the moment the engine first fires.

The Elite Advantage in Funding

Our long-standing relationships with specialty lenders provide a distinct advantage for our clients. We streamline the often-complex documentation required for custom build and restoration labor fees, ensuring the full value of the craftsmanship is recognized by the bank. This professional coordination saves you time and preserves your liquidity. For a deeper dive into specific loan products and structures, you can explore our dedicated Classic Car Financing pillar. We act as the bridge between your long-held dream and the tangible reality of a high-performance restomod.

From Dream to Driveway

The journey concludes with a seamless delivery experience that reflects the quality of the build itself. Our turnkey approach includes Enclosed Vehicle Transport to ensure your new acquisition arrives in showroom condition, regardless of the distance. We handle the logistics so you can focus on the drive. Taking the next step is simple. Whether you are looking for a pre-approval to act quickly on a rare find or want to browse our current inventory of investment-grade icons, our team is ready to assist. We invite you to consult with our financing specialists today to begin your journey toward owning a masterpiece of modern performance and vintage soul.

Drive Your Vision into Reality

The 2026 collector market demands a fusion of financial intelligence and automotive passion. You’ve seen how strategic leverage preserves liquidity and how a meticulously documented build book overcomes the appraisal hurdle. It’s about moving beyond the limitations of traditional banking to embrace a partnership that understands the heartbeat of a restomod. Financing a six-figure classic car is the final component in a build process that treats every gear and stitch as a bespoke piece of functional art. Raw power. Refined comfort.

Our partnerships with premier specialty lenders ensure your capital is deployed with the same precision we apply to our chassis engineering. Every vehicle in our stable carries the Elite Certified seal of quality; this provides the transparency that underwriters and appraisers require. From climate-controlled storage to nationwide enclosed transport, we manage the intricacies of your acquisition so you can focus on the visceral thrill of the drive. The bridge between your long-held dream and a high-performance reality is ready. Your next investment-grade icon is waiting for its first mile.

Explore Our Elite Certified Inventory and Financing Options

Frequently Asked Questions

Can I finance a restomod that has a modern engine and chassis?

Yes, specialty lenders recognize that modern performance upgrades like fuel-injected engines and precision chassis enhance the collateral value of the vehicle. Unlike traditional banks that rely on outdated depreciation models, these partners value the reliability and engineering of a bespoke build. This understanding is what makes financing a six-figure classic car possible for collectors who prioritize the driving experience over strict originality.

What is the typical down payment required for a six-figure classic car?

You should expect to provide a down payment of 10% to 20% for most high-value automotive acquisitions. This initial capital stake establishes immediate equity and demonstrates your commitment to the asset’s preservation. For loans exceeding $100,000, a 20% down payment is often the standard for securing the most competitive Tier 1 interest rates and the most flexible terms.

How long are the loan terms for a $100,000+ collector vehicle?

Loan terms for elite collector vehicles frequently extend up to 180 months, providing a level of flexibility not found in standard auto loans. These 15-year terms are designed to minimize the impact on your monthly cash flow while you enjoy the vehicle’s appreciation. Most specialty lenders require a minimum loan amount of $100,000 to qualify for these extended amortization schedules that preserve your liquid capital.

Does financing a classic car require a different type of insurance?

Lenders mandate agreed value insurance to ensure the full investment is protected against total loss. Unlike standard policies that use actual cash value, agreed value coverage locks in a specific dollar amount based on a professional appraisal. This is a non-negotiable requirement for financing a six-figure classic car because it protects both your equity and the lender’s collateral from market depreciation.

Can I finance a vehicle that I am commissioning as a custom build?

Commissioned builds can be financed through specialized progress payment loans or by securing a loan once the vehicle reaches a specific stage of completion. Lenders require a comprehensive build book and a contract with a reputable master builder to approve these requests. The loan is typically structured around the anticipated final market value of the functional art piece you are creating.

What happens if the appraisal comes in lower than the purchase price?

If the appraisal is lower than the purchase price, the borrower typically covers the difference with a larger down payment. This gap often occurs when the cost of artisanal labor and high-end components exceeds the basic comparable sales data available to the appraiser. Utilizing professional consignment data from recent high-profile auctions can often help bridge this gap during the underwriting process.

Are there prepayment penalties for high-value classic car loans?

Most premier specialty lenders don’t charge prepayment penalties, allowing you to settle the debt at any time without extra fees. This feature is vital for collectors who treat their garage as a rotating portfolio of assets. It provides the freedom to sell the vehicle or trade up to a higher-tier restomod whenever the right opportunity appears in the market.