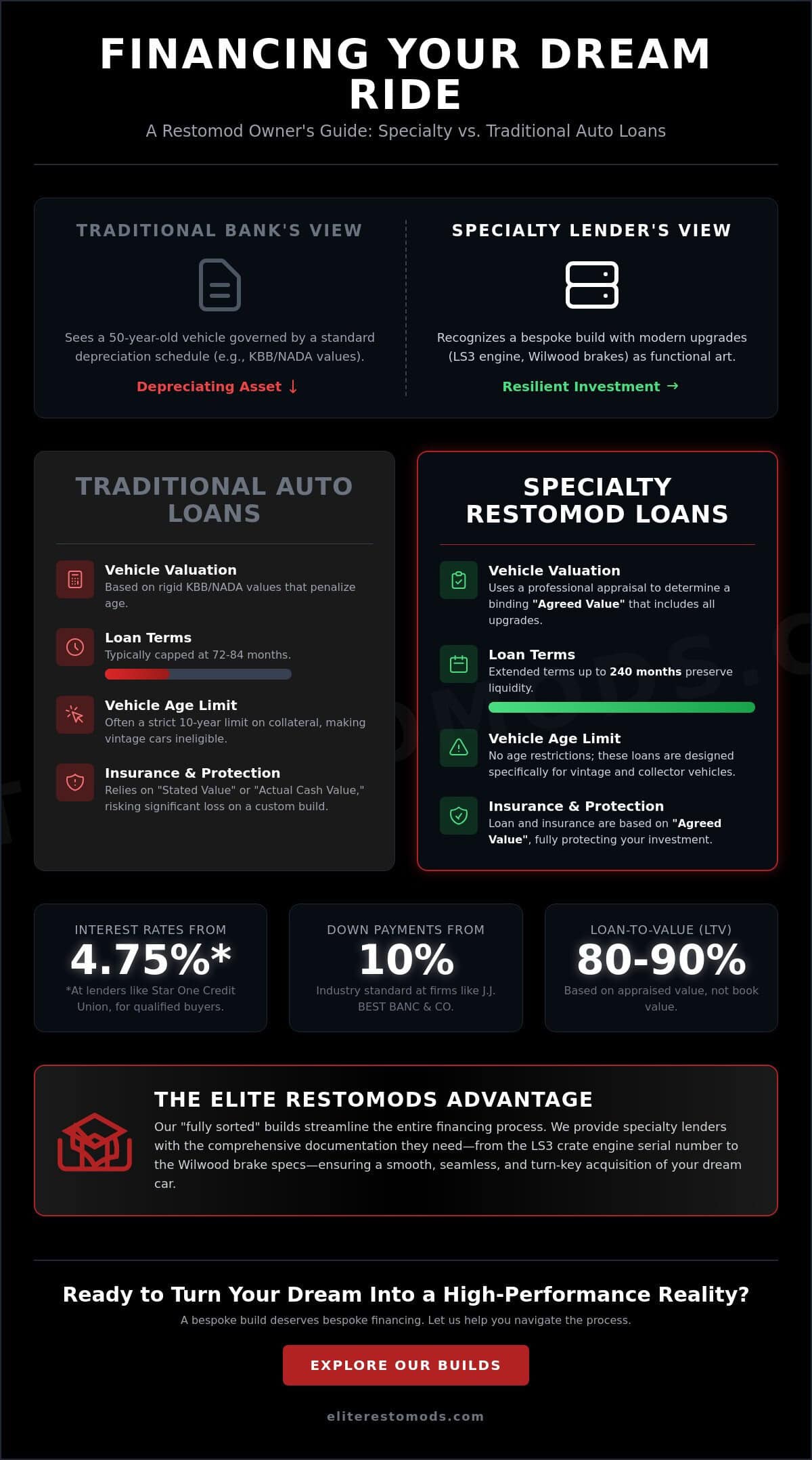

Why would you ask a banker who specializes in commuter sedans to value a hand-built 1969 Camaro pushing 650 horsepower from a fresh LS3 crate engine? Most enthusiasts realize that traditional lenders see a vintage masterpiece as just an old car with a high price tag. They don’t understand the soul of a restomod. If you’re wondering how do classic car loans work, the answer lies in specialty lenders who recognize that a bespoke build is functional art, not a depreciating asset. These institutions understand that while the Hagerty Market Rating sits at 59.01 as of March 2026, the value of a meticulous restoration remains resilient.

You deserve a financing partner that respects the marriage of vintage style and modern reliability. This guide reveals how to secure terms up to 240 months and navigate interest rates that start as low as 4.75% at Star One Credit Union. We’ll explore why a 10% down payment at J.J. BEST BANC & CO. might be your ticket to the driver’s seat and how agreed value protection keeps your investment safe. From technical appraisals to seamless acquisitions, you’ll learn how to turn your childhood dream into a tangible, high-performance reality.

Key Takeaways

- Understand why traditional depreciation schedules don’t apply to restomods and how specialty lenders value your vehicle’s modern performance upgrades.

- Learn exactly how do classic car loans work by utilizing professional appraisals and “agreed value” structures to protect your bespoke investment.

- Identify the specific credit score and debt-to-income benchmarks required to unlock premium 2026 interest rates and extended loan terms.

- Compare the advantages of specialty collector financing against personal loans to determine the best path for your specific build or acquisition.

- Discover how the “fully sorted” nature of an Elite Restomod build streamlines the financing process for a seamless, turn-key delivery.

What is a Classic Car Loan and Why is it Different?

A classic car loan is a precision financial instrument. Unlike a standard note on a daily driver, it’s built to respect the unique trajectory of a collector vehicle. While a new SUV loses approximately 20% of its value the moment it leaves the lot, an iconic muscle car often moves in the opposite direction. The definition of a classic car can vary by state or club, but for a lender, it represents an asset class that defies the standard rules of gravity. These specialty products allow collectors to acquire high-value assets without liquidating their entire portfolio.

Understanding how do classic car loans work requires shifting your perspective from transportation to investment. These loans are designed for vehicles that are appreciated, not just used. For a high-performance restomod, the loan isn’t just covering a chassis; it’s financing the raw power of an LS3 crate engine and the precision of Wilwood brakes. Specialty lenders view these machines as functional art. They recognize that while the Hagerty Market Rating dropped to 59.01 in early 2026, the top end of the market featuring rare, bespoke builds remains incredibly strong.

To better understand this concept, watch this helpful video:

The Limitations of Traditional Banks

Standard banks are built for the predictable. They rely on rigid NADA or Kelley Blue Book values that simply cannot account for the immense value hidden beneath a vintage skin. If a bank sees a 1967 Mustang, they see a 60-year-old car. They don’t see the hand-stitched interior or the modern performance suspension. Most traditional institutions also enforce a strict 10-year age limit on collateral. This makes it nearly impossible to finance a vintage icon through a local branch. At Elite Restomods, our meticulous build process creates a “fully sorted” vehicle that provides the documentation specialty underwriters need to bypass these traditional hurdles.

Specialty Lenders: The Collector’s Ally

Specialty firms like Woodside Credit or J.J. BEST BANC & CO. act as curators of the financial world. They understand the “Coyote-swap” value add. They don’t flinch at a six-figure price tag for a vintage silhouette because they know the mechanical intricacies involved. These lenders offer “Agreed Value” coverage. This ensures the loan and insurance reflect the actual replacement cost of the build, not a generic market average. By utilizing terms that can stretch to 240 months, these loans preserve your liquidity. You keep your capital in other investments while you enjoy the visceral roar of a high-performance beast.

How Classic Car Loans Work: The Mechanics of the Deal

Securing financing for a high-performance restomod requires more than just a credit check. It’s a technical evaluation of the machine’s soul. When people ask how do classic car loans work, they’re often surprised by the depth of the valuation process. Unlike standard auto loans that use “Stated Value,” which is essentially what you tell them it’s worth, specialty lenders rely on “Agreed Value.” This is a legally binding figure determined by the purchase price or a professional appraisal. It ensures that if your bespoke 1970 Chevelle is totaled, you’re covered for the actual cost of the build, not its 50-year-old scrap value.

The appraisal is the backbone of the entire transaction. A certified professional must verify the mechanical upgrades, paint quality, and overall structural integrity. For those researching how to get a classic car loan, this step is non-negotiable. Lenders typically offer a Loan-to-Value (LTV) ratio of 80% to 90%. For example, Star One Credit Union often finances up to 80% of the average CPI value. This results in a 10% to 20% down payment requirement, which is the industry standard for investment-grade assets in 2026. Interest rates currently range from 4.75% to over 15% depending on the lender and your credit profile.

The Importance of the Build Sheet

Your build sheet is your leverage. Documentation of a modern LS3 crate engine, Wilwood brakes, or a Tremec six-speed transmission isn’t just for car shows; it’s for the underwriter. These components add tangible value that specialty lenders recognize. A “fully sorted” vehicle with a documented history is far easier to finance than a mystery project. When you browse our current inventory of bespoke builds, you’ll see the level of detail that lenders find irresistible.

Down Payments and Equity

Cash is king, but equity is a close second. While a 10% down payment is common at institutions like J.J. BEST BANC & CO., the condition of the car dictates the final terms. A pristine, “Elite Certified” restomod may qualify for longer terms, such as 120 or even 240 months, which keeps monthly payments manageable. Understanding how do classic car loans work through the lens of equity and down payments allows you to build a collection that is both a thrill and a sound financial move. Collectors often use equity from an existing stable of vehicles to bridge the gap, treating their garage as a revolving investment fund. This strategic approach ensures you have enough skin in the game while maintaining the liquidity needed for your next acquisition.

Comparing Your Options: Specialty Loans vs. Alternatives

Choosing the right financing is as critical as selecting the right powerplant for your build. While there are several paths to ownership, not all are created equal in the eyes of a collector. To truly understand how do classic car loans work, you must compare them against the broader financial landscape. A specialty loan is a precision tool. It’s designed for the unique appreciation curves of iconic muscle cars, whereas general alternatives often treat your investment like a disposable commodity.

Personal loans offer a common alternative, but they come with trade-offs. These are typically unsecured, meaning the lender doesn’t use the vehicle as collateral. In early 2026, rates at lenders like LightStream range from 6.49% to 15.24% APR. This “cash buyer” position provides significant leverage at auctions, yet the lack of a lien means you miss out on the specialized valuation an underwriter provides. Furthermore, personal loans rarely offer the extended 144-month or 240-month terms that make high-value acquisitions affordable. You are effectively trading long-term cash flow for short-term convenience.

Other collectors consider Home Equity Lines of Credit (HELOC) or straight cash purchases. A HELOC can offer competitive rates, but it secures your 1969 restomod against your primary residence. This creates an unnecessary layer of risk for a luxury asset. Cash is the simplest route, but it carries a heavy opportunity cost. Tying up significant capital in a static asset prevents you from deploying those funds into other high-yield investments. In a market where approximately 70,000 classic cars are sold annually, maintaining liquidity is a tactical advantage.

Specialty Lenders vs. Personal Loans

Specialty loans provide a distinct edge by using the car as collateral. This allows institutions like Star One Credit Union to offer rates as low as 4.75% APR for vehicles listed in the CPI Price Guide. Because the lender understands the “LS-swap” value add, they are comfortable with longer horizons. A personal loan is a sprint, often capped at 60 or 72 months. A specialty loan is a long-distance tour, offering the breathing room to enjoy your investment while your capital works elsewhere.

Why a Dedicated Classic Car Loan Wins

A dedicated loan mandates specialized “agreed-value” insurance. This is your ultimate safety net. It ensures your investment is protected at its true, appraised worth rather than a depreciated book value. These loans also simplify the process if you choose to sell the vehicle later, as the documentation is already tailored for the collector market. For a deeper look at why these vehicles are increasingly viewed as stable assets, see The 2026 Guide to Restomod Car Investment. It’s about more than just a monthly payment. It’s about protecting the soul of your machine.

Qualifying for Classic Car Financing in 2026

Entering the world of high-performance restomods requires a financial profile as polished as a show-quality finish. While some niche lenders consider scores as low as 600, securing the most competitive 2026 interest rates requires a credit score typically between 700 and 740. Lenders also scrutinize your Debt-to-Income (DTI) ratio with precision. They want to see that your passion for American muscle doesn’t compromise your overall financial stability. Understanding how do classic car loans work means recognizing that lenders are evaluating your reliability just as much as the machine’s mechanical integrity.

Beyond the numbers, two non-negotiable hurdles exist: specialty insurance and a professional inspection. Most specialty lenders require an “agreed-value” policy before they’ll release a single dollar. This isn’t just red tape. It’s a mutual protection of the vehicle’s meticulous restoration value. Additionally, a third-party inspector must verify the “bones” of the car. They look for structural excellence and verify that the LS3 crate under the hood matches the build story provided. This ensures the asset is worth the investment before the roar of the engine ever leaves our shop.

Preparing Your Financial Portfolio

High-limit loans for six-figure builds demand total transparency. You’ll likely need tax returns from the last two years and statements showing your liquid assets. A clean driving record is also essential. It directly impacts your ability to secure the required specialty insurance. Review the full list of Classic Car Loan Requirements to ensure your financial portfolio is ready for the underwriter’s meticulous review. Preparation today leads to a faster turn-key reality tomorrow.

The Role of the Dealership

We treat the financing process with the same perfectionism we give to our hand-stitched interiors. Elite Restomods acts as the bridge between your childhood dream and the lender’s technical requirements. We provide the comprehensive build sheets and performance specs that underwriters need to justify the vehicle’s unrivaled value. This collaboration often leads to “Elite Certified” funding approvals in as little as 48 hours. We handle the complexities of out-of-state titles and lien placements. This makes the acquisition process as seamless as a Coyote engine at idle. Ready to find your next masterpiece? View our current selection of high-performance builds today.

Financing Your Elite Restomod: Performance Meets Investment

An Elite Restomod is more than a vehicle. It’s a verified asset. Lenders often hesitate when a build is shrouded in mystery, but our “Fully Sorted” status changes the conversation entirely. When underwriters see the documentation for our investment-grade inventory, they see a machine with unrivaled reliability and turn-key performance. This transparency is the secret to understanding how do classic car loans work for high-end builds. It transforms a complex negotiation into a straightforward approval based on documented excellence. By choosing a vehicle that has undergone a meticulous restoration, you provide the lender with the confidence they need to offer extended terms and lower down payments.

Structured payments turn the visceral roar of a Coyote engine from a distant dream into a daily reality. Financing allows you to preserve your capital for other high-growth opportunities while you enjoy the immediate sensation of 600 horsepower. This approach also simplifies your eventual exit strategy. Whether you choose to move into a different model through a trade-in or place your car in a future consignment sale, having a documented financial history and a recognized valuation makes the transition seamless. In a market where online auctions now account for nearly 70% of all classic car sales, having a “fully sorted” and financed asset positions you as a sophisticated player in the collector community.

A Bespoke Experience from Build to Bank

We believe the financial acquisition should be as refined as the hand-stitched leather in our interiors. Classic style meets modern financial power through our specialized approach. We don’t just build cars; we curate the entire ownership journey. This includes matching the mechanical sophistication of your vehicle with a professional lending experience that respects your time and your portfolio. You can explore our financing services for custom builds to see how we tailor the process to your specific vision. Every detail matters, from the Wilwood brakes to the interest rate on your note.

Take the Next Step Toward Your Icon

The “Elite” difference in the 2026 collector market is defined by reliability and perfectionism. While the broader market might feel flat with a Hagerty rating of 59.01, the demand for unrivaled restomods continues to climb. Our team is ready to provide referrals to trusted lending partners who truly understand how do classic car loans work for bespoke machinery. They recognize the soul of vintage American muscle and possess the vision to value modern engineering. For a deeper dive into the technicalities of these financial products, read our Financing Pillar Article. Your childhood dream is waiting. Let’s put it in your garage.

Master Your Automotive Legacy

Bridging the gap between a childhood dream and a high-performance reality requires more than just passion; it demands a sophisticated financial strategy. You now understand that while traditional banks struggle to value bespoke craftsmanship, specialty lenders offer the 240-month terms and competitive 4.75% rates that make these icons accessible. Navigating how do classic car loans work is the final step in securing an asset that defies standard depreciation. By prioritizing “agreed value” and leveraging professional appraisals, you ensure your investment remains as resilient as the 70,000 collector cars sold annually in this active market.

At Elite Restomods, we eliminate the friction of acquisition. Our “fully sorted” vehicles come with comprehensive documentation, providing the clarity that our industry-leading lending partners require for rapid approval. We treat every build as a piece of functional art, ensuring its modern engineering is matched by a professional lending experience. The roar of a precision-tuned engine is within reach. Take the next step toward a turn-key masterpiece that balances raw power with refined elegance.

Secure Your Dream: Explore Our Elite Certified Inventory and Financing Options

Frequently Asked Questions

What is the minimum credit score for a classic car loan?

A credit score of 700 or higher is the standard benchmark for securing premium interest rates in 2026. While specialty lenders like Collector Car Lending may consider applicants with scores as low as 600, the most favorable terms are reserved for those with a 740 or above. Higher scores unlock the liquidity needed for high-performance restomods and ensure the most competitive 4.75% APR entry points.

Can I finance a restomod that has a modern engine swap?

Yes, specialty lenders specifically cater to vehicles featuring modern performance upgrades like LS3 crates or Coyote engines. Unlike traditional banks, these institutions recognize the unrivaled value of modern reliability paired with vintage aesthetics. Documenting these meticulous mechanical upgrades is a core part of understanding how do classic car loans work for the restomod market.

How long are the terms for a collector car loan?

Terms for investment-grade vehicles can extend up to 240 months. Lenders like LightStream and J.J. BEST BANC & CO. offer these 20-year horizons to keep monthly payments manageable for six-figure acquisitions. This flexibility allows you to enjoy the visceral roar of your machine while preserving your capital for other bespoke investments.

Do I need a down payment for a classic car loan?

Most specialty lenders require a minimum down payment between 10% and 20% of the vehicle’s value. Star One Credit Union typically finances up to 80% of the CPI value, which necessitates a 20% equity stake from the buyer. This initial investment serves as a safeguard for both the lender and the collector’s long-term portfolio.

Is a classic car loan better than a personal loan?

A specialty loan is generally superior because it offers “agreed value” protection and significantly lower interest rates. Personal loans are unsecured and can carry rates as high as 15.24% as of early 2026. By using the vehicle as collateral, you gain access to underwriters who truly understand how do classic car loans work to protect your asset’s bespoke value.

Does the car need to be inspected before the loan is approved?

Yes, a professional third-party inspection is a standard requirement for most specialty lending products. The inspector verifies the structural integrity and mechanical specifications, such as Wilwood brakes or custom suspension, to ensure the car is “fully sorted.” This technical verification provides the foundation for the loan’s final approval and the vehicle’s insurance policy.

Can I use a classic car loan for a vehicle I’m commissioning to be built?

Certain specialty firms offer bespoke stage-funding or “build-out” loans specifically for custom commissions. These products allow for financial disbursements as the restoration hits specific milestones, such as the final paint finish or engine installation. It acts as the bridge between your initial childhood dream and the final, high-performance reality.

What happens if the appraisal comes in lower than the purchase price?

If the professional appraisal fails to meet the purchase price, you must cover the difference in cash or renegotiate the sale terms. Lenders base their Loan-to-Value ratios strictly on the appraised “agreed value” to mitigate risk. This is why choosing a builder with documented industry credibility and a history of high-end sales is essential for a seamless acquisition.